The traditional approach to calculations often results in an estimate of the actual costs of complex products that is too low. Fast-moving products tend to be calculated too expensively and slow movers too cheaply. This can lead to poor strategic decisions, resulting in the erosion or complete loss of profits. As the variants become more complex, the lack of knowledge regarding the costs and expenses involved becomes increasingly apparent. Sales errors and declining productivity in the manufacturing process can also result. Here, a practical, systematic procedural model can provide valuable help. Knowing the actual costs and expenses is the key to optimisation that leads to increased productivity and a reduction in lead times for orders.

The calculation of configurable products is a key pillar in the configuration and quoting process and is an important contributor to a company’s success. The author, Uwe Metzger, is an expert on the subject and explains here how common mistakes can have expensive consequences, and how to avoid them.

Traditional cost accounting

In traditional cost accounting, the production costs of technical products are usually, at least to a certain extent, calculated using planned contribution margins. The individual cost items are charged with percentage overhead rates, and these form the mean values for the calculated expenses. Development, warehousing and logistics expenses, and also a proportion of production costs, are often calculated using overhead rates.

Miscalculations using overhead rates

Many years of experience in comparing marginal costing with the distribution of actual costs for multi-variant products in the capital goods sector have shown that the calculated figures for fast-moving product variants produced in large numbers are usually too high, and for the slow-movers produced in small numbers too low.

A manufacturer of packaging machines, for example, was shown to have overestimated the costs of the standard product for a packaging plant by 18% using the traditional costing approach. The estimation for a special variant of the product, however, was 86% too low when compared to the actual costs.

The risk of strategic error

I have seen the effect described above with many suppliers of capital goods. As a result, the proportion of special solutions increases steadily and the profit margins are gradually eroded.

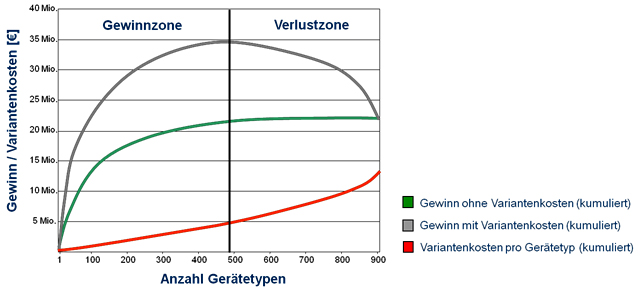

The actual costs of product variants produced in small numbers usually greatly exceed the calculated costs. The diagram above shows the calculated profits and losses of a manufacturer with more than 900 product variants. A comparison is shown between the company’s performance based on traditional marginal costing and a cause-based calculation using variant costs.

The grey curve represents the actual profits and losses for the individual product variants, accumulated over one year. It can clearly be seen that the product variants on the right result in losses for the company!

The pitfalls of an approach that ignores the actual variant costs are obvious: Variants are developed and produced at great expense in small numbers – variants that not only tie up important company resources, but also contribute to an overall loss or at best lead to diminished profits.

I have experienced companies whose order books are full but who still make a loss, and who are never entirely sure which products and product groups are primarily responsible for this. The lack of transparency regarding the actual distribution of the costs opens the door for strategic miscalculations in a company.

Things start to get dangerous at the point where sales are increasingly generated by special products which cause real loss of profit.

Cause-based calculations are important right from the quotation stage

Many successful producers of plants and capital goods are used to developing machines tailored to their customers’ individual requirements. Their motto seems to be that the customers can have exactly whatever they want – as long as they pay for it.

There is no denying that a high level of customer-friendliness and individuality of products are a key success factor for many manufacturers. This does, however, result in increasingly complex products. Modern plants consist of highly-complex mechanical components, new technologies and materials in combination with sensors, activators, motors and electronic controls. And increasingly often, specific connections to consoles and adjustments to the control panel are required. The cost of developing and implementing specific adjustments thus continues to rise.

It is therefore all the more important to calculate the costs of the required adjustments on a cause basis right from the quotation stage. Only in this way can a situation be avoided in which the internal costs and effort required for a new order exceed the estimations, and lengthy delays to the delivery occur.

Supporting Sales

Sales staff for plants and capital goods tend to be overwhelmed by the increasing complexity of today’s integrated systems. Even highly-experienced employees from technical sales are becoming less able to assess the overall impact of individual changes. Seemingly minor adjustments for the customer can thus produce major unplanned implementation costs.

The systematic documentation and classification of product variants together with the cost of the necessary adjustments and resources is therefore increasingly important as a basis for planning and calculating the costs of new orders in a cause-based way.

To ensure the best support for the quotation and order process, the sales department needs a system that guides the user through the sales process. It should take into account both the technical and functional dependencies and use the actual costs as a calculation basis.

Rethink established procedures

The continuing increase in individual product solutions and in particular the increasing product complexity means that manufacturers have to rethink established procedures that were successful in the past in order to maintain their competitiveness in the coming years.

Imagine a manufacturer that produces several hundred different variants each year. The development costs and effort involved in the design, approval and transfer to production will vary greatly for each type of variant. With several hundred variants yearly, it is no longer practical for engineering employees to document the exact number of hours spent on a project or to precisely allocate resources to each order and calculate the costs individually. At best, very rough estimates of the expenditure can be produced.

It is a similar situation with expenditure in logistics. Depending on the scale of the necessary adjustments, special variants will normally mean that new materials have to be sourced, imported, stored and assigned to production for each order. The special materials and materials sourced in very small amounts lead to increased costs and effort in the whole logistics chain: material planning, ordering, receipt of goods, material tracking, transport of material, storage, material allocation, and provision of spare parts. Here as well, no allocation of expenditure to the product variants is normally possible due to the wide variety of different materials used.

Additional expenditures for special materials for the production range from the creation or adaptation of NC programmes and adjustments to auxiliary equipment and tools, to the equipping and setting up of the machines and the preparation of production documents. Special variants also lead to queries and indeed to errors in production which reduce productivity even further.

Providing a basis for optimisation

A simple and practical procedural model can be used to systematically analyse the costs and bottlenecks generated by product variants.

This is an excellent basis for making further optimisations in the company. These may involve adjustments to the calculation of costs for product variants, increasing productivity in development and production, or decreasing the lead times for customer orders.

Founder and owner, I&R Innovation & Results, Assling near Munich

LinkedIn